Table of Content

Performance information may have changed since the time of publication. If you want coverage for earthquake-related problems, consider an earthquake insurance policy. The majority of homeowners who have flood insurance buy it through the federal plan managed by FEMA, but you can potentially buy flood insurance from a private insurer.

Take the square footage cost for your home, and add in the cost to replace your roof, cabinets, and attached appliances. This yields an approximate dollar amount for rebuilding your home, which is likely a different amount than you paid for it. This amount is the minimum amount of dwelling coverage you need to ensure you can rebuild your home in the event of a total loss. Buy or renew your policy to prevent any unnecessary damages to ensure you have adequate homeowners insurance coverage at all times. Your policy should also be adjusted as soon as possible when you make changes like home renovations or the purchase of a new home.

Average homeowners insurance costs

Whether you have a repair estimate or not, you can contact your homeowners insurance company and file a claim for the roof damage. You will need to fill out paperwork explaining what caused the damage, what type of damage occurred when the event happened and what else was damaged as a result . You should also include the repair estimate if you have one, and any photos or videos of the damage for evidence. You may want more coverage than the amount it would likely cost to rebuild. You might need to make changes to your house to bring it up to code.

More expensive medical claims would be covered under liability insurance. This pays for minor injuries to others if they’re hurt on your property. This coverage is usually sold in small amounts, often between $1,000 and $5,000.

What does dwelling coverage not cover?

For example, an extended replacement cost policy might provide an extra 25% above your dwelling coverage, if needed. For example, If you have $300,000 in dwelling coverage, extended replacement cost at 25% would provide up to $375,000 total to rebuild the house. Structures that aren’t attached to your house, like a fence or shed, are covered under the “other structures coverage” portion of a homeowners insurance policy.

These are just general guidelines for what is included in dwelling coverage, so read your policy closely to know exactly what it does — and does not – cover. “These calculators factor in the price of goods and labor in your ZIP code, along with features of the house which include square footage, quality unique features,” he says. Dwelling policy coverage also include attached structures, such as your garage, as well as built-in features such as chimneys and porches. Even if you aren’t planning to sell, it’s worth considering replacing your roof if the roof is near the end of its life.

Find the Best Homeowners Insurance Companies Of 2022

A dwelling is an insured structure that is covered by dwelling insurance. For example, dwelling home insurance would cover the home itself, but not other structures on the property such as a shed or a fence. This is the preferable method of valuation for homeowners because it adds up how much it will cost to replace each of the lost structural features. Instead of your insurance paying out the value of your 10-year-old roof, for instance, you are paid for the amount to install a new roof of the same type. If there is doubt about what is and isn’t protected under dwelling coverage, ask your home insurance agent for clarification. Insurance companies are able to determine the amount of dwelling coverage based on factors such as square footage, garage type, number of fireplaces, and many other considerations.

This is the reason your agent is going to ask a ton of questions. We don't want you being left short-changed if your home needs to be rebuilt and you want to have your home look as much like your previous home as possible regarding finishings. Manufactured home insurance in the U.S. generally ranges from $500 to $1,100 per year, according to American Modern Insurance Group, a prominent mobile home insurer. Many or all of the products featured here are from our partners who compensate us.

What can I get dwelling insurance for?

Even after you figure out the right amount, you should update your policy periodically. It is also possible to get an inflation guard endorsement that will increase your dwelling coverage limit annually to keep it in line with inflation. For example, if the river in your town swells and floods your home, you will not be covered because flood damage isn’t covered by a standard homeowners insurance policy. Similarly, if an earthquake causes structural damage to your home, the damages won’t be covered by homeowners insurance.

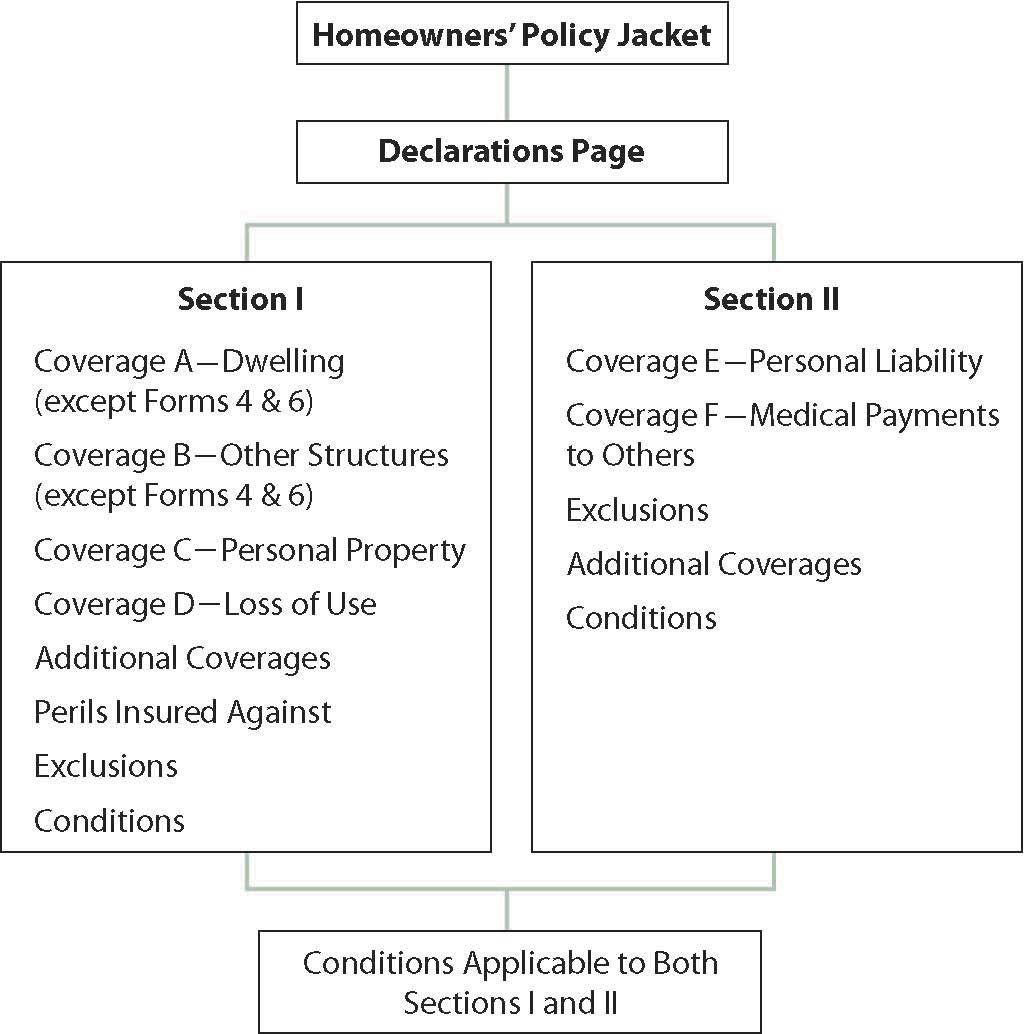

Dwelling coverage is the part of homeowners insurance that covers damages to the physical structure of the policyholder’s home due to a covered peril. It provides protection against potentially significant expenses should it be necessary to rebuild the home. The right amount of coverage varies per person and will depend on individual needs. MoneyGeek breaks down what dwelling coverage is and how you can determine the amount of coverage suitable for you. Extended replacement cost coverage gives you some cushion when the cost to rebuild your house goes above your dwelling policy limits. This coverage can be particularly useful if your region is hit by a widespread disaster that causes a spike in local costs of materials and labor.

Dwelling coverage does not protect you in the event of a flood, which is defined as an event that covers at least two acres or affects two properties. To get this type of coverage, you would need to purchase a separate flood insurance policy. For example, if a tornado sweeps in and destroys an entire neighborhood, the cost of labor and materials to rebuild could soar. In such situations, extended dwelling coverage can provide the extra insurance you need to repair or rebuild your home. In some cases, you may want to purchase coverage beyond the full replacement cost of your home. Your home insurance company may pay for repairs if a tree falls onto the roof or a section of shingles blows off in a storm.

You should talk to your insurance agent to determine the right amount — but as a general rule, your homeowners insurance should cover the full cost to replace your home. That means you should purchase coverage in a dollar amount equivalent to 100% of the cost of rebuilding your home from scratch. For example, if a hailstorm or the weight of snow after a blizzard damages your roof, a home insurance policy will likely pay for the repairs or a new roof. You don’t need to purchase a special type of insurance for roof replacement, but you can buy a home warranty that may help you with repairs not covered by homeowners insurance. So, what is dwelling coverage and what does homeowners insurance help cover?

No comments:

Post a Comment